what happens to 529 when child turns 21

From a financial perspective, i of the best things to come up out of the coronavirus-induced market meltdown is being able to contribute to your children'south 529 plans at lower index prices. Let us dig deep into the recommended 529 plan amounts by age.

The appropriate 529 plan amounts by age will help ensure that you accrue enough to pay for your child's college education comfortably. At the aforementioned time, the right 529 plan amount by age volition also ensure that you don't over-invest if you don't want to.

Given parents are investing for an expense that might not occur for some other 10-18 years, it's easier to invest in a 529 plan during times of turmoil. You want to have the right about in a 529 programme by age and so you don't overfund or underfund the college savings account.

Investing In My Daughter's 529 Programme

Originally, I had but planned to invest $15,000 into my girl's 529 plan in 2020 considering I was nervous about the stock market after a 10-year bull run. All the same, in one case the stock market started selling off in Feb and March 2020, I decided to contribute more to her plan. See my 529 contributions beneath.

The stock market kept on tanking until I ran out of the maximum bullets immune. By the end of March 2020, I had concluded up superfunding $75,000 into my daughter's 529 program. Afterwards making a stock market bottom prediction in March 2020, I put my coin where my mouth was and bought.

If I had contributed more, I would have violated the superfunding rule, which allows families to front-load v years worth of contributions ($75,000 per donor/$150,000 per couple) without having to file gift taxes, while protecting their lifetime gift and estate tax exemption.

Given the world felt similar it was coming to an terminate in March 2020, my wife and I decided to have her dollar-cost-boilerplate into our girl's 529 plan by $15,000 a year for the adjacent five years but in case the recovery takes years.

When the stock market place began rebounding in April, so did both of our children'south 529 plans. Today, our son'southward 529 programme account is only about twice as large, despite beingness 3X older.

This is when I began to wonder what is the advisable 529 program amounts past age. I was commencement to feel similar nosotros had over-contributed to our daughter'south 529 plan. Nevertheless, thanks to the probable incessant rise in college tuition, continuing to contribute to a 529 savings plan makes sense.

Why A College Degree Is Getting Devalued

One of the most important things all parents and kids who want to attend higher should know is this: Partly due to the coronavirus, the value of college has declined.

While this decline in value has been ongoing for years and started well before COVID-xix arrived, with tens of millions of people sheltering in place for months, the depreciation has accelerated.

A student or parent should not take to spend the same corporeality of tuition for classes that are being taught online instead of in the physical classroom. An important office of the college experience is in-person networking to build lifelong connections and friendships. Moving online impedes this invaluable opportunity.

It is already likewise late for many of usa who accept spent big bucks and many years getting our higher degrees. However, it is not too tardily for our children to brand wiser educational and fiscal decisions about their higher teaching.

If we do nil, and then we will be creating another generation of massively indebted and highly dissatisfied higher graduates who are unable to discover meaningful work. Debt and a lack of meaningful work hurt relationships, delay saving and investing, delay or eliminate family germination, and create deep levels of dissatisfaction.

Nosotros all know some messed up, angry people. They could have had better lives if they weren't and then burdened by educatee loan debt and had more enjoyable occupations.

Central Points On Instruction:

- Online education devalues a traditional higher pedagogy.

- Information technology is nonsensical for a educatee to still accept to spend four-5 years before being awarded a higher diploma when the cyberspace has made inquiry, learning, and advice much quicker.

- Unless you are already rich or receive grants, paying full individual school tuition is fiscally unwise considering data shows that there is no discernible income departure between both types of higher graduates from private or public schools.

- Even public school tuition is becoming too expensive given a consistent decline in state-supported funding. No type of education is increasing in value.

- From a financial standpoint, it'southward more than benign to learn everything for complimentary online, develop skills in a high need field, take an apprenticeship, and get to work sooner after high schoolhouse.

Recommended 529 Plan Amounts Past Age Framework

To come up up with my recommended 529 plan amounts by age, we must make several assumptions. I will provide three columns to accost these assumptions. Then yous tin can follow the cavalcade that most closely matches your state of affairs and beliefs.

529 Plan Assumptions:

- You are a rational parent who likes to have advantage of revenue enhancement-advantageous accounts to potentially grow your investments quicker. You believe that if you are going to invest for your kid's education, and so you might besides invest in a 529 programme where the contributions compound tax-free.

- The contribution range per year is between $five,000 and $30,000. The range takes into account contributions from single parents, dual-income parents, grandparents, and rich relatives.

- The compounded return range is betwixt 0% – seven%. This range accounts for bear markets and lower returns as child gets closer to attending college. Lower returns are due to a greater shift to bonds.

- The goal is to pay for between 50% – 100% of college expenses when the time comes. The pct range takes into consideration parents who do not take as much money or have lower investment returns. The lower percentage as well accounts for parents who want their children to have more skin in the game.

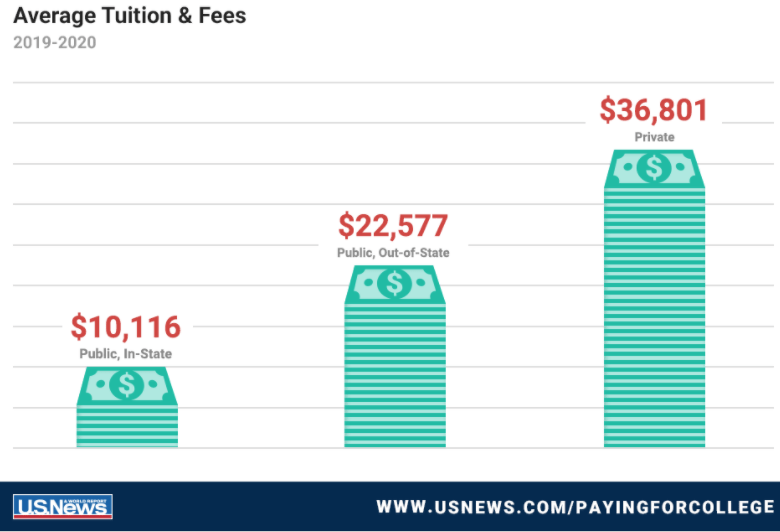

- For 2020, the average public tuition & fees cost is ~$ten,500 a year for public-instate, ~$23,000 a year for public, out-of-state, and ~$37,000 for private universities co-ordinate to US News & World Report. Expect these tuition figures to go up by almost iv-five% a yr forever.

More 529 Plan Assumptions:

- College tuition and expenses will increase by an boilerplate of 3% a year, fifty-fifty though the value of college is failing. It is very hard to terminate momentum, specially due to growing international demand.

- Some of the 529 plan may exist used to pay for form school tuition and expenses. As of 2020, $10,000 a year can exist used from a 529 plan per student per year for private, public or religious elementary, middle, and loftier school tuition.

- Financial support for teaching stops at 25. Age 25 is old enough for a kid to have started and finished a Principal's caste. It is also old enough for the adult child to become on the path to financial independence. You plan to spend downwards 100% of the 529 plan after 25 years.

- Contributing too much is an inefficient apply of funds because the money could besides be spent on living a improve life.

Now that nosotros have these assumptions in place, permit'due south look at the recommended 529 plan amount by age.

Recommended 529 Program Amounts By Historic period

Below is my recommended 529 plan amounts past age separated into iii columns. Each of the columns accounts for the type of school your child plans to go to and how much financial assistance your family unit will receive.

For most new families, I advise focusing on the Medium (Bravo) column.

Depression Column (Alfa)

The Depression column simply assumes a $5,000 contribution per yr with 0% growth to account for several bear markets during the initial xviii years. The goal is to have saved $100,000 per child by the time he or she begins college. Starting at xviii, the parent uses $20,000 a year to pay for higher pedagogy expenses.

Those who should follow the Low column:

- Parents who have older children already (ten+)

- Parents don't believe strongly in the value of a college didactics

- Child volition go to a public university, community college, 2-year college, or potentially no college

- Kid is a genius or a talented athlete and will get tuition subsidies from universities

- Guardians have a family business

- Parents have many children and cannot fully fund all their 529 plans

Medium Column (Bravo)

The Medium column assumes a $xv,000 annual contribution every yr until xviii with a 6.ii% chemical compound almanac return. The goal is to have saved $500,000 per child by the fourth dimension he or she begins college. Subsequently historic period eighteen, $100,000 a yr is to pay for college until the 529 plan goes to 0 at historic period 25.

Those who should follow the Medium cavalcade:

- Parents or guardians take a newborn or children nether three

- Guardians or parents but plan to have i or two children

- Parents believe a college pedagogy is still valuable

- Child is of average intelligence and athletic ability

- Guardians or parents desire to hedge confronting a continued rapid increase in college tuition

- Parents or guardians take a family business

- Parents tend to exist more financially bourgeois

Loftier Column (Coca)

The High column assumes a $30,000 annual contribution every year until 18 with a 7% compound almanac return. The $30,000 comes from a combination of two people always contributing $fifteen,000 each.

The two people tin can be both parents, one parent and a grandparent, two grandparents, and so forth. After 18, $200,000 a yr is used for college tuition until the 529 plan is spent down to $0 at age 25.

Those who should follow the High column:

- Parents accept a newborn or a kid who has withal to be born

- Parents plan on just having 1 or two children

- Child is of beneath average intelligence and athletic ability

- Child insists on going to the most expensive private schoolhouse

- Parents are very wealthy and are willing to brand their children 529 millionaires

- Parents believe college tuition will inflate much faster than 5% a year

- Grandparents have enough coin to superfund their grandchildren'south 529 plans to help reduce their estate

- Parents who desire to use the 529 plan as a generational wealth transfer vehicle

Each column represents the appropriate amount based on your goals and your child'due south educational goals. All columns are great goals to follow. The amounts should align with your goals and beliefs.

If you're backside, contribute more than. Or convince a grandparent or relative to contribute more. If y'all're ahead, throttle your contributions and apply your money for other purposes.

It would be irrational if you relieve based on the Low cavalcade but take a child who is one year old and yous want him to go to the virtually expensive university in xviii years without any grants.

It would also be irrational to follow the High column if your child is already 14 years old, is bright, and will likely get a gratis ride to any schoolhouse she chooses.

Whichever column yous cull to follow, make sure the numbers align with your current fiscal situation. Empathize your child'southward intelligence and work ethic. Know your beliefs most college pedagogy.

Related: Recommended 401(k) Amounts By Age

529 Plan Amounts By Historic period Goals For My Children

My married woman and I are personally going to shoot to save up to $500,000 per child by the time each turns xviii. In other words, we program to contribute a combined $xv,000 a yr and hope for roughly a half dozen.25% compound annual return. Our goal is inline with the Medium (Bravo) column.

Worst example, if our children are not smart enough to attend an in-state public academy or don't become grants from a individual university, so nosotros are looking at between $100,000 – $125,000 a yr all-in per kid.

The cost is based on a 5% compound aggrandizement rate for the next 15-eighteen years. $500,000 per kid in a 529 plan will be able to cover this realistic worst-case scenario.

Every bit our children get older, we will accept a better thought of their intelligence levels and work ethic. Nosotros can then adjust our contributions accordingly.

My wife and I have always been of average intelligence. Therefore, our children will likely have the aforementioned level of intelligence. We cannot count on instilling in our children a strong ethic, no matter how hard we attempt.

Whether you follow my Low, Medium, or High 529 plan savings amounts past age, know that investing in a tax-advantageous business relationship for your children is better than not investing in one.

Using A 529 To Transfer Wealth

Ideally, you desire to save just the right amount in each 529 programme. Just if you finish up saving too much, you lot can always just reassign the beneficiary. The beneficiary tin exist reassigned to your grandchildren or someone else for generational wealth transfer purposes.

Finally, in addition to building a large enough 529 plan for your kids, consider also opening up a custodial Roth IRA. By putting your kids to work, they can contribute to a Roth IRA likely tax-costless.

The money will then compound tax-free over fourth dimension. After 5 years, your kid tin can then withdraw the coin revenue enhancement-free to spend on whatever they want!

If y'all first your child'southward Roth IRA early, I'm sure they will exist ecstatic when they get adults.

Diversify Into Real Estate

It's also bad parents tin can't invest in real manor in a 529 program. Real manor is my favorite asset class to build wealth given the combination of rising rents and rising capital values. This combination tends to build tremendous wealth over time.

That said, you tin invest in real estate through a REIT, private eREIT, or physical rental properties. Personally, I've invested in all three as real estate accounts for 40% of my net worth. Stocks make upwards xxx% of my net worth.

Since 2016, I've been investing consistently in existent estate crowdfunding to have advantage of lower valuations in the heartland of America. With more people relocating to lower-cost areas of the country, I believe the heartland will see multiple decades of growth.

Take a look at Fundrise, my favorite existent estate crowdfunding platform. Fundrise has diversified eREITs that provide 100% passive income and diversification. For virtually people, investing in a fund is the easiest fashion to gain exposure.

As well take a look at CrowdStreet, a great real estate platform that focuses on individual deals in eighteen-hour cities. If you have more capital, you can build your own select fund with CrowdStreet. They've got a neat platform with very intriguing deals.

Both platforms are complimentary to sign up and explore. I've personally invested $810,000 in 18 real estate crowdfunding deals so far.

Readers, what is the right 529 plan amounts past age you lot're going to follow? Personally, I think the recommended 529 programme amount is between $300,000 – $500,000 for each child.

Source: https://www.financialsamurai.com/recommended-529-plan-amounts-by-age/

0 Response to "what happens to 529 when child turns 21"

Post a Comment